You land a new client. The contract is ready. Then comes the email: “Please send us a certificate of insurance before we can move forward.” If you’ve been in business for any amount of time, you’ve seen this request. Maybe you knew exactly what to do. Or maybe you stared at it, unsure what they were actually asking for and what happens if you can’t deliver. You’re not alone. A certificate of insurance (COI) is one of the most requested business documents, yet many small business owners are unclear on what it is, why clients need it, and how to get one quickly. This guide breaks it all down.

What is a Certificate of Insurance (COI)?

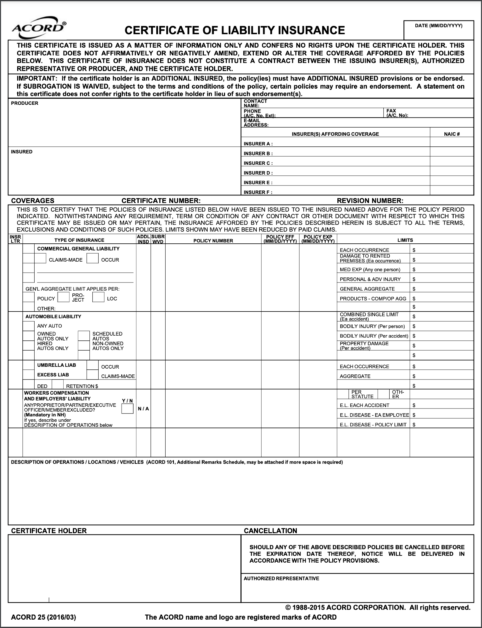

A certificate of insurance is a one-page document that summarizes your insurance coverage. It’s not a policy itself. Think of it as a snapshot that proves your insurance exists. A standard COI includes:

- Your business name and contact information

- The name of your insurance company

- The types of coverage you carry (general liability, commercial auto, workers’ comp, etc.)

- Your policy numbers

- Coverage limits for each policy

- Policy effective and expiration dates

- The name of the “certificate holder,” typically the client or vendor requesting it

The most common form used in the U.S. is the ACORD 25, a standardized certificate recognized across virtually every industry.

Why Do Clients and Vendors Ask for a COI?

The short answer: they want proof you’re covered before you set foot on their property or start work on their project. Here’s why that matters to them:

- They don’t want to be held liable for your accidents. If something goes wrong on their job site or property, such as an injury, property damage, or a lawsuit, a client could be dragged into it if you don’t carry adequate insurance.

- Many contracts legally require it. Construction contracts, commercial leases, vendor agreements, and government contracts routinely include insurance requirements as a condition of doing business.

- Lenders and property managers require it. If you rent a commercial space or work with a general contractor, a COI is often a non-negotiable part of the agreement.

- It protects their business, too. A client who verifies your coverage before work begins reduces their own exposure. It’s a standard business practice, not a sign of distrust.

When a client or vendor asks for a COI, it’s a good sign. It means they’re serious about the working relationship.

What is an “Additional Insured” and Why Does It Matter?

You may notice that some clients don’t just want a COI. They want to be listed as an “additional insured” on your policy. This goes a step further than simply proving you have coverage. Being listed as an additional insured means that client receives certain protections under your liability policy if a claim arises from your work. It’s a common requirement for general contractors, property owners, and large commercial clients. If a client requests this, your insurance agent can add them as an additional insured through an endorsement on your policy. It’s a routine request, but it does require a specific update to your policy, not just the certificate itself.

What Happens If You Can’t Provide a COI?

Simply put, you may not get the job. Many clients and general contractors will not allow work to begin until they receive a valid COI. If your coverage has lapsed, you carry insufficient limits, or you’re missing the required type of coverage, you could:

- Lose a contract to a competitor who is properly insured

- Be removed from a job site or vendor list

- Face delays that cost you time and money

- Be in violation of a signed contract

Beyond the business impact, operating without adequate insurance puts your personal and business assets at risk if something goes wrong on the job.

How Do You Get a Certificate of Insurance?

If you already have a commercial insurance policy, getting a COI is straightforward. Your insurance agent or carrier can typically generate one within 24 hours often the same day. Here’s what you’ll need to provide when requesting one:

- The name and contact information of the certificate holder (your client or vendor)

- Any specific coverage requirements they’ve outlined (minimum limits, required coverage types)

- Whether they need to be listed as an additional insured

- The project or contract details, if relevant

The faster you can supply this information, the faster your agent can get the certificate back to you. One important note: a COI is only as current as your policy. If your insurance lapses or you reduce your coverage, any existing certificates become void. Keeping your policy active and up to date is the only way to ensure your COI remains valid when clients request one.

How AIS Insurance Helps You Stay Ready

At AIS Insurance, we understand that a delayed COI can mean a delayed job or a lost one. If you’re unsure whether your current policy meets the requirements your clients are asking for, or if you need to get coverage in place quickly, we can help. Call AIS Insurance today at (866) 570-7335 to speak with a licensed commercial insurance specialist. We’ll review your needs, make sure your coverage is solid, and ensure you can provide a COI the next time a client asks.

The information in this article is obtained from various sources and offered for educational purposes only. Furthermore, it should not replace the advice of a qualified professional. The definitions, terms, and coverage in a given policy may differ from those suggested here. No warranty or appropriateness for a specific purpose is expressed or implied.